Income of non-resident people. Withholding taxes are taxes that are deducted from the source.

Extended Withholding Tax Sap Simple Docs

Withholding tax is an amount withheld by the resident carrying on business in Malaysia on income earned by a non-resident and paid to the Inland Revenue Board of Malaysia.

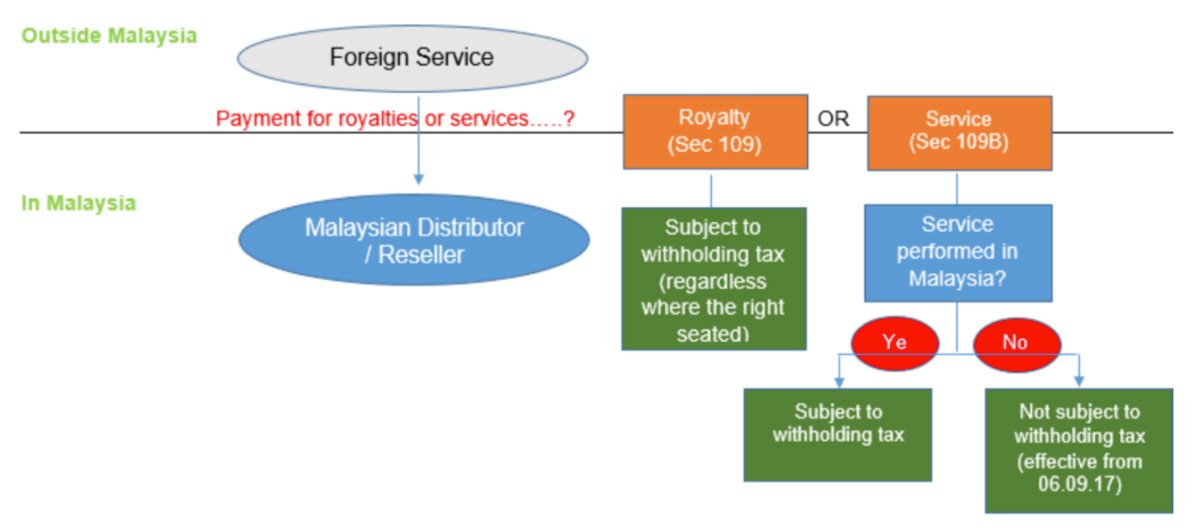

. Any non-resident company receiving income from the use of or right to use software or the provision of services. Payer refers to an individualbody other than individual carrying on a business in Malaysia. The Exemption Order exempts a non-resident from the payment of income tax in respect of certain categories of income derived from Malaysia under certain circumstances and stipulates that the withholding tax obligations under Section 109B of the Malaysian Income Tax Act 1967 Act will not be applicable to the exempted income.

Demystifying Malaysian Withholding Tax. Contract payments to non-resident contractors are subject to a total withholding tax of 13 10 for tax payable by the non-resident contractor and 3 for tax payable by the contractors employees. It includes payments such as.

Withholding tax is applicable on payments for certain types of income derived by non-residents. These guidelines have adopted features from the Multilateral Instrument MLI to implement treaty. Each payment will have a separate withholding tax rate and if Malaysia and the country in which the non-resident is a tax.

RM100000 01 RM10000. Affected business modelsin-scope activities. Withholding tax is an amount withheld by the party making payment payer on income earned by a non-resident payee and paid to the Inland Revenue Board of Malaysia IRB.

The Malaysian Income Tax Act 1967 ITA 1967 provides that where a resident is liable to make payment as listed below other than income of non-resident public. Payments for the use of any item carried such as rent or other fees. It goes back to the Income Tax Act of 1969.

Payer refers to an individualbody other than individual carrying on a business in Malaysia. 8 2022. 78 rows Any tax resident person who is liable to make certain specified types of payments to a non-resident is required to deduct withholding tax at a prescribed rate applicable to the gross payment and remit it to the Malaysian IRB within one month of paying or crediting.

Let us assist you to demystify the changes made to the withholding tax provisions and support you in complying with your withholding tax obligations particularly. Ibu Pejabat Lembaga Hasil Dalam Negeri Malaysia Menara Hasil Persiaran Rimba Permai Cyber 8 63000 Cyberjaya Selangor. The responsibility for deducting and remitting the withholding tax lies with the Malaysian payers.

The tax rate payable for royalty payments is 10 of the gross amount. The payer must within one month after the date of payment to the non-resident remit the withholding tax to LHDN. -Visitors This Month.

8 2022 -Visitors This Month. Headquarters of Inland Revenue Board Of Malaysia. Withholding tax is an amount withheld by the resident carrying on business in Malaysia on income earned by a non-resident and paid to the Inland Revenue Board of Malaysia.

Failing of doing so you may face the potential risks of. Withholding taxes are taxes that are deducted from the source. How to pay Withholding Tax in Malaysia and penalty if not paid.

Download Form - Withholding Tax. Ibu Pejabat Lembaga Hasil Dalam Negeri Malaysia Menara Hasil Persiaran Rimba Permai Cyber 8 63000 Cyberjaya Selangor. Headquarters of Inland Revenue Board Of Malaysia.

Withholding taxes are withheld by the party making payment payer on income earned by a non-resident payee and paid to the Inland Revenue Board of Malaysia LHDN. Since the Malaysian withholding tax provision places significant demands and. Revenue stream in scope.

Withholding tax is an amount withheld by the party making payment payer on income earned by a non-resident payee and paid to the Inland Revenue Board of Malaysia. Withholding tax in Malaysia is not new. 7 2022 -Visitors This Year.

The withholding tax provisions under the Act place tremendous demand on payers and hence a good understanding of the Malaysian withholding tax regime is critical to avoid any potential on non-compliance penalties. He is required to withhold tax on payments for services renderedtechnical. The following countries have concluded double tax treaties with Malaysia.

The Malaysian Income Tax Act 1967 ITA 1967 provides that where a resident is liable to make payment as listed below other than income of non- resident public. On 21 May 2020 the Inland Revenue Board of Malaysia IRBM has issued guidelines to provide clarification in determining a place of business PoB of a non-resident person in Malaysia. The source would usually be other countries.

Section 109 1 of the ITA requires withholding tax to be deducted from royalty payments derived from Malaysia and payable to a non-resident. -Visitors This Month. A any sums paid as consideration for the use of or the right to use.

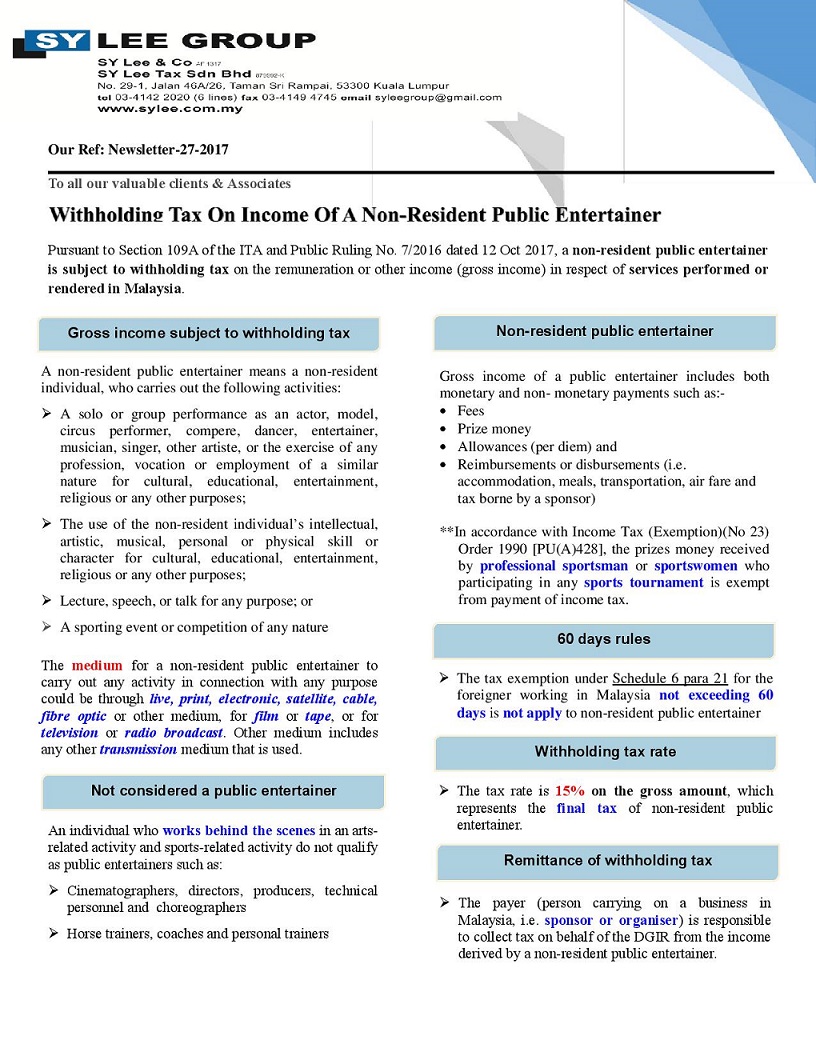

Malaysian withholding tax applies to certain payments made or credited to non-Malaysian tax residents if the payments are derived from or deemed to be from Malaysia. Income derived in Malaysia by a non-resident public entertainer is subject to a final withholding tax at a rate of 15. Royalty is defined in Section 2 of the ITA and includes -.

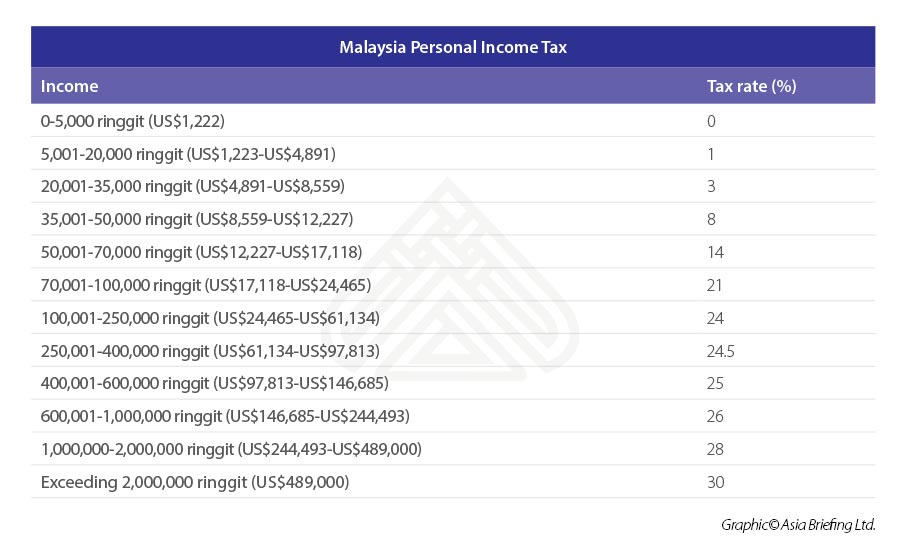

Tax Rates

Newsletter 65 2018 Withholding Tax On Special Classes Of Income Page 002 Jpg

Ayks Management Services 帖子 Facebook

Individual Income Tax In Malaysia For Expatriates

Asiapedia Key Tax Rates In Cambodia Dezan Shira Associates

Tax Rates

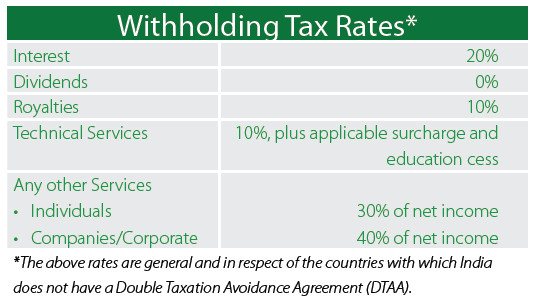

Asiapedia Withholding Tax Rates In India Dezan Shira Associates

2

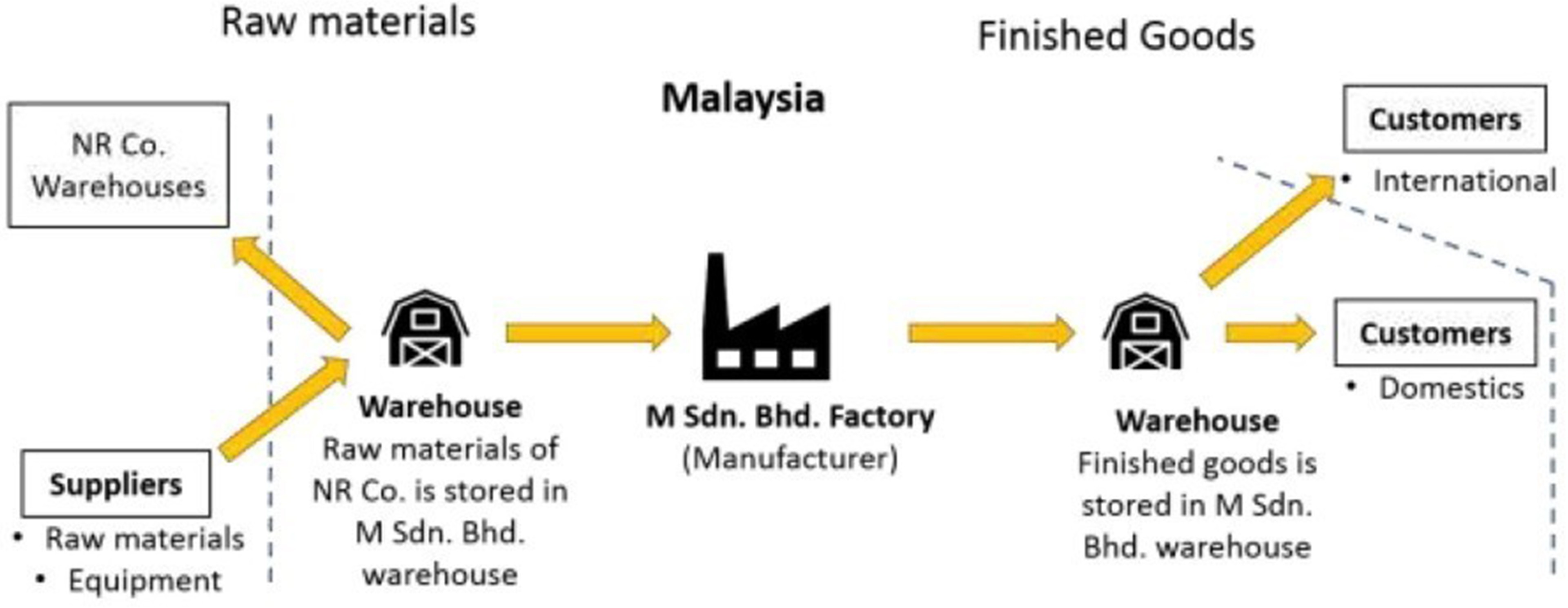

Guidelines On Determining If A Place Of Business Exists In Malaysia Ey Malaysia

Extended Withholding Tax Sap Simple Docs

Extended Withholding Tax Sap Simple Docs

Newsletter 27 2017 Wht On Income Of A Non Resident Public Entertainer Page 001 Jpg

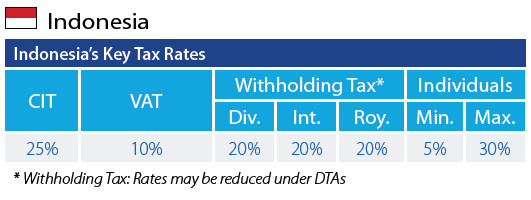

Asiapedia Key Tax Rates In Indonesia Dezan Shira Associates

Purpose Of Certificate Of Residence Under Withholding Tax In Malaysia Apr 23 2021 Johor Bahru Jb Malaysia Taman Molek Service Thk Management Advisory Sdn Bhd

2 Withholding Tax For Agent Commission Cp107d Form Lhdn

Introduction To Withholding Tax Imported Services Tax Part 2

Extended Withholding Tax Sap Simple Docs

Newsletter 27 2017 Wht On Income Of A Non Resident Public Entertainer Page 002 Jpg

Tax Rates